Secretary Bessent is Wrong on State Tax Conformity

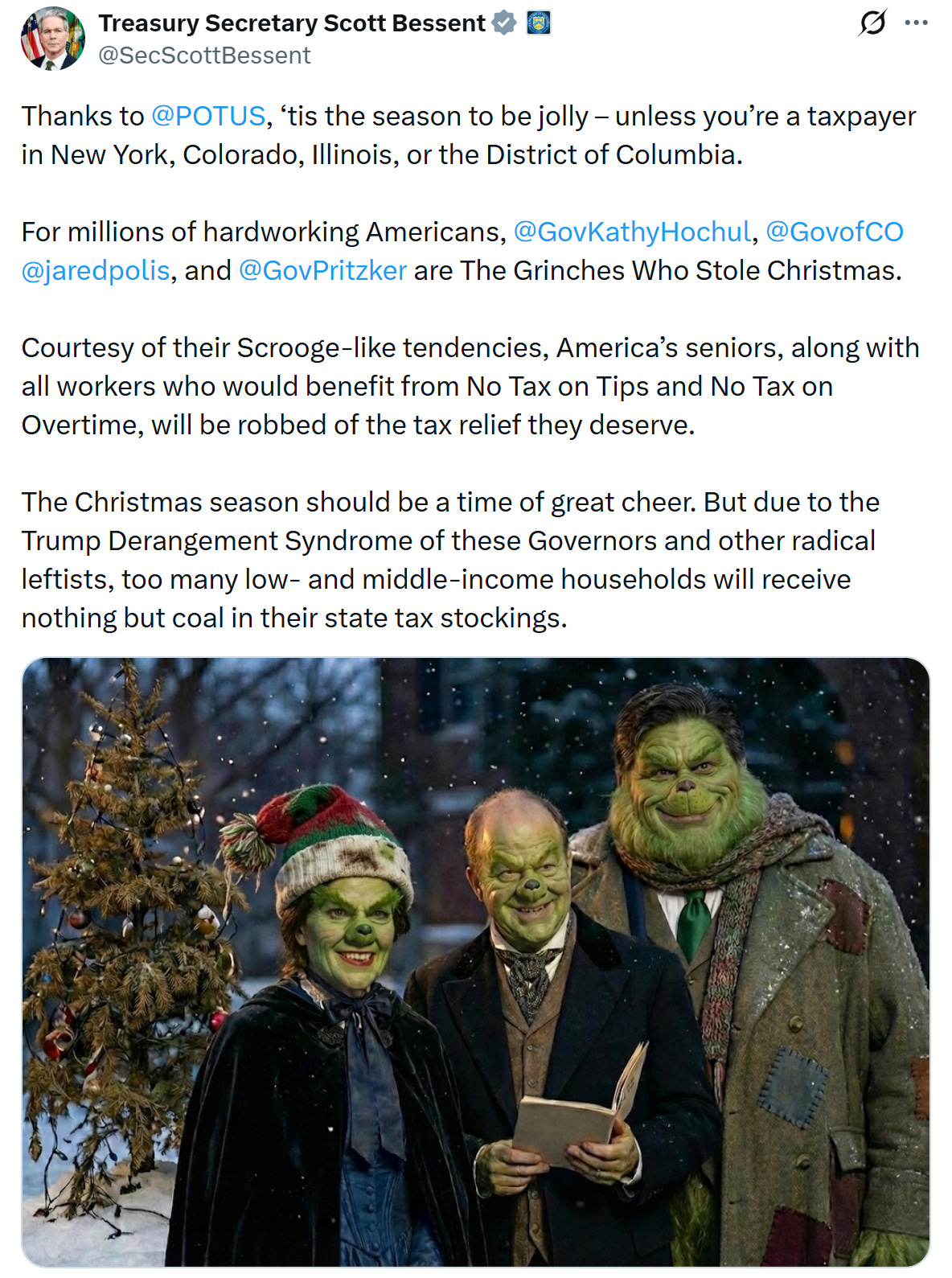

Treasury Secretary Scott Bessent believes that some blue state governors deserve a lump of coal in their stockings this Christmas for “rob[bing]” people of tax relief:

This is wrong—very wrong.

Secretary Bessent doesn’t say that states’ policies could reverse the benefit of the new federal provisions, but I’ve now had multiple people tell me they’ve heard that message, so let’s be abundantly clear: whether or not a state incorporates these deductions into their own tax codes, they’re not doing anything to deprive their taxpayers of the full benefit of the federal deductions.

What Bessent does say is that a coterie of elected officials in New York, Colorado, Illinois, and the District of Columbia are thwarting state-level tax relief. It’s an odd list because it’s so capricious and incomplete. Only eight states are currently in line to bring in some or all of these new provisions: seven because the state’s tax code begins with federal taxable income rather than adjusted gross income, and one (Michigan) through legislation expressly conforming to the new deductions for tips and overtime, and the new senior bonus. To Bessent’s list, you could add every state with a Republican governor except those in the five Republican-led states that use federal taxable income as their income starting point.

In other words, New York Gov. Kathy Hochul, Illinois Gov. JB Pritzker, and D.C. Mayor Muriel Bowser haven’t done anything at all. They simply haven’t championed adopting these deductions voluntarily, just like most of their gubernatorial peers, including most Republican governors.

Colorado, meanwhile, is one of the seven states that begin their tax calculations with federal taxable income. While lawmakers made a few tax changes in a recent special session, they left the deductions for tips and vehicle loan interest alone, along with the new enhanced senior deduction. (Earlier, Colorado preemptively decoupled from the overtime pay deduction.) Governor Jared Polis, therefore, is the rare governor presiding over a state that does offer most of these deductions, yet he inexplicably makes Bessent’s naughty list.

These deductions are temporary, arbitrary, costly, and confer little economic benefit. There’s no compelling reason why a low- or middle-income tipped employee should pay less income tax than a non-tipped worker making the same amount. Similarly, it’s not obvious why overtime pay should receive better treatment than ordinary wage income, or why the tax code should put a thumb on the scale in favor of taking out larger car loans.

Conversely, the restoration of full expensing of machinery and equipment under § 168(k) and of research and experimentation costs under § 174 is extremely high-impact tax policy, yet the Secretary has trained his ire on (select) states that don’t proactively adopt these non-neutral personal deductions rather than on the states that actively decouple from neutral cost recovery.

As I’ve written elsewhere, the OBBBA gets business expensing right, and states should follow suit. You’d think these far more economically salient policies would be the ones worthy of the Treasury Secretary’s attention.

Obligatory Marketing Note

My new consultancy provides tax policy research, writing, and other services. If you are in the market for tax policy research or know someone who is, please let me know.

A Request: Please Share This Substack

If you find this Substack valuable, please do me a favor and share it with colleagues and others who may be interested, either by forwarding this to them or using the “share” button below. And if you haven’t yet subscribed (it’s free), please consider doing so!

States not incorporating these changes to taxable income is no problem. A much bigger pain is Virginia decoupling from the SALT limit but then reintroducing Pease. I greatly hope that Virginia conforms on the new 2/37 limitation (which is superior to Pease and actually achieves the stated goal) instead of continuing to have a separate Pease calculation.